What's Behind the Unexpected EUA Price Fluctuations This Summer?

Amid summer heatwaves, potential strikes, and a surge in renewables, the EUA market faces unpredictable shifts with implications for Europe's energy landscape.

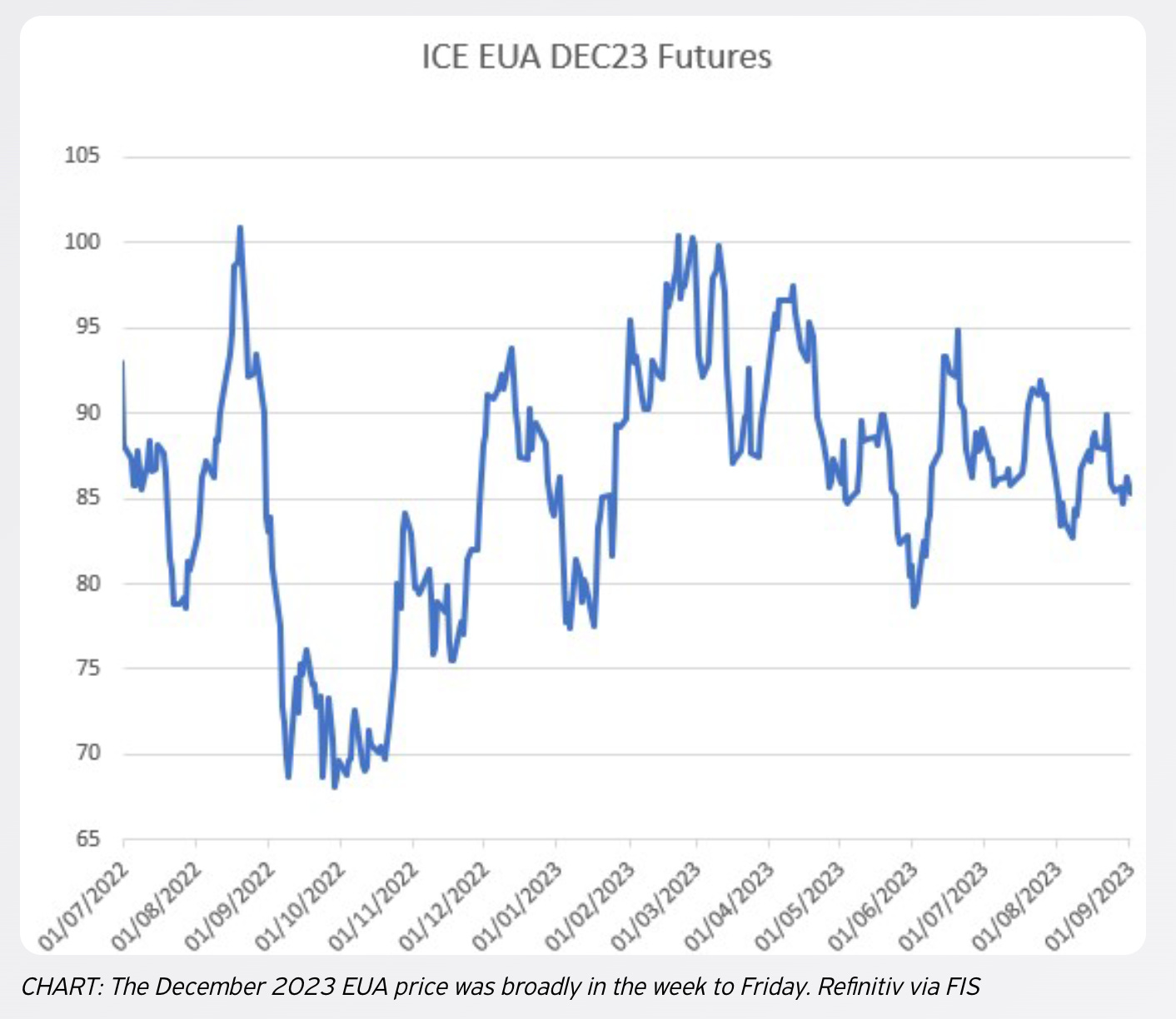

The European Union Allowance (EUA) market, a crucial component of the EU's emissions trading scheme, experienced a series of ebbs and flows last week, closing almost flat at EUR 85.27. This minuscule dip of 0.14% mirrors a period characterized by a lowered auction volume throughout August and changing weather patterns, notably reduced temperatures in Southern Europe.

On Tuesday, prices for the benchmark Dec-23 EUA contract fluctuated between EUR 85.40 and EUR 86.48, predominantly as reactions to potential strikes at Chevron’s LNG facilities in Australia, even though the lion's share of the gas from these plants mainly serves the Asian market. Mirroring this, the prices of physical EUAs during auctions settled at EUR 84.64.

But as always, investor activities have the power to alter the winds. With the Wednesday release of the Commitment of Traders (CoT) report indicating a slight uptick in short positioning from investment funds, the Dec-23 saw an uptrend of 1.7%, landing at EUR 86.24.

As August curtains closed and the hum of post-summer vacation activities started to pick up, compliance buying gave a gentle nudge to emission prices. The Dec-23 EUAs momentarily touched EUR 86.95 on Thursday, later setting for the day at EUR 85.76.

Friday, ushering in September, witnessed an auction volume reminiscent of 2021 – over 3 million EUAs on offer. However, the Dec-23 seemed reluctant to venture far from EUR 86.00.

Interestingly, August marked a decline in EUA prices, a trend not observed since 2019. What's been the catalyst? A floundering gas market appears to be a central protagonist, with gas prices taking a significant dip. This reduction in gas demand inevitably trickled down to EUAs, culminating in a final reduced auction volume.

Combine this with reports indicating a 5% YoY fall in EU power generation for the first half of the year and the soaring 23% increase in renewable power generation. Gas burning, on the other hand, has seen a slump of 13%. The resultant effect? A dip in EUA demand and a surge in short positions from speculative traders.

However, the horizon offers intriguing possibilities. The transition from August's halved auction volume could see prices stabilize or even spike momentarily due to reduced auction activities in the coming week. But this stabilization might be fleeting. The full-blown return of auctions and the cooling down of Southern Europe might nudge EUA prices downwards in September, a sentiment echoed by several prominent EUA analysts.

Supporting this potential decline, recent statistics have spotlighted the meteoric rise in renewable capacity in the EU, which coupled with a 20% decline in power emissions, may foreshadow a fall in EUA prices in the approaching months.

Upcoming weeks will also experience a surge in the supply of EUAs to the market. From 6.2 million mt this week, a whopping 14.6 million mt is set to be auctioned in the week commencing 11 September.

Moreover, Bloomberg's own analysts predict a potential dip in European emissions for the remainder of 2023. Paired with the increased auction volumes, this could lead to an oversupply in the market, exerting a downward thrust on EUA prices. Additionally, high European gas storage levels since 2022 hint at a more than adequate gas supply for the upcoming colder months.