EUAs Stirred by Gas Prices: A Week of Twists and Turns

Gas Prices, Short Squeezes, and Global Shifts: Navigating a Week of Carbon Market Whirlwinds

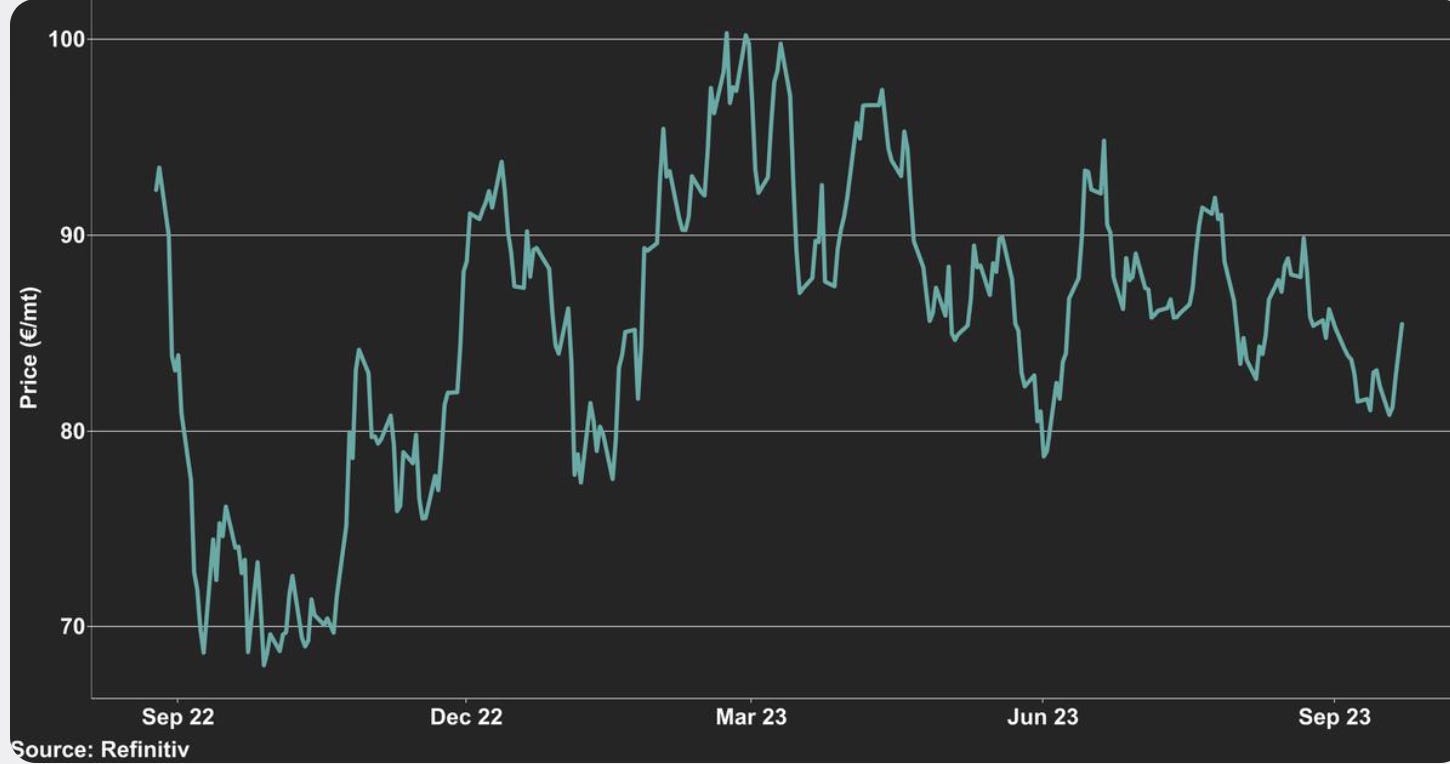

Price Movements: A Wild Ride

In the past week, the European carbon market has been nothing short of a roller coaster. Opening the week, EUA prices seemed to relinquish their gains from the prior week. The Dec23 contract climbed to a morning high of EUR 82.65 on Monday, only to backtrack and close the day at EUR 80.84, a low not seen since June.

The market played a waiting game on Tuesday, oscillating in response to the upcoming Intercontinental Exchange (ICE) quarterly option contract expiry and the Commitment of Traders (CoT) data. Despite trading between EUR 81.23 and EUR 80.55, EUA prices managed to return to their morning highs, settling at EUR 81.23.

Wednesday witnessed the climax of the drama. The expiry of the quarterly options contract combined with the CoT data revealing an increase in net short positioning led to a rush in EUA prices, reaching EUR 82.80. Thursday only amplified the momentum, as a robust auction turnout led to a surge of 40 cents above the spot price. In a mere 15 minutes, the EUAs experienced a bump of EUR 1.50, finishing the day at a two-week high of EUR 84.14.

Riding the bullish wave, Friday's trading reached a three-week peak of EUR 86.13, with the Dec23 contract signing off at EUR 85.48.

(Benchmark Dec 23’ Contract up 4% intraday)

Market Drivers: What's Fueling the Flames?

At the week's start, EUA prices appeared to echo the weakness in the EU gas markets. With the TTF price plummeting by 6% on Monday, the clean dark spread was inching close to zero, hinting at a potential profitability switch from coal to gas. Yet, as the week advanced, gas prices rebounded, influencing an EUA rally.

The CoT data on Wednesday proved to be a pivotal factor. Revealing that investment funds had bolstered their net short position to 21.8 million EUAs, the market was reminded of a similar scenario in June, where a short squeeze led to an EUR 18 price surge.

Post the September options contract expiry on Wednesday, the soaring demand in Thursday's auction could be attributed to short covering or, as some suggest, triggered by dip buyers. A significant external factor was the truce between Chevron and the unions, which concluded strikes at two LNG plants in Australia. With attention refocusing on the North Sea, both natural gas and EUA prices ascended.

Future Outlook: Clear Skies or Stormy Weather Ahead?

While the short-term outlook is tinted with bearish hues—attributed to high auction volumes, speculative short positioning, and dampened demand—there's an undercurrent of long-term bullish sentiment. This optimism is pinned to 2026, marking the end of the REPowerEU front-loading and other supply tweaks.

Moreover, power sector hedging remains a critical determinant for EUA prices. With the World Meteorological Organization forecasting the return of the El Nino phenomenon, weather predictions will gain prominence, shaping the EUA landscape in the months ahead.

In conclusion, the European carbon market this past week was a testament to its dynamic nature, influenced by various internal and external factors. Whether these trends persist or shift, one thing is certain: stakeholders will be watching closely, ready to adapt to the ever-evolving carbon landscape.