A Week of Declines and Uncertainties in the Carbon Markets: EUAs, UKAs, and Beyond

A Week of Declines and Uncertainties in the Carbon Markets: EUAs, UKAs, and Beyond

Navigating the Tides of Change: Unpacking the Latest Movements in Global Carbon Markets

In a week marked by significant movements across various carbon markets, the European Union Allowances (EUAs) and UK Allowances (UKAs) have both witnessed notable declines. This article delves into the dynamics of these markets, exploring the factors driving these movements and their implications.

European Union Allowances: A Downward Trend

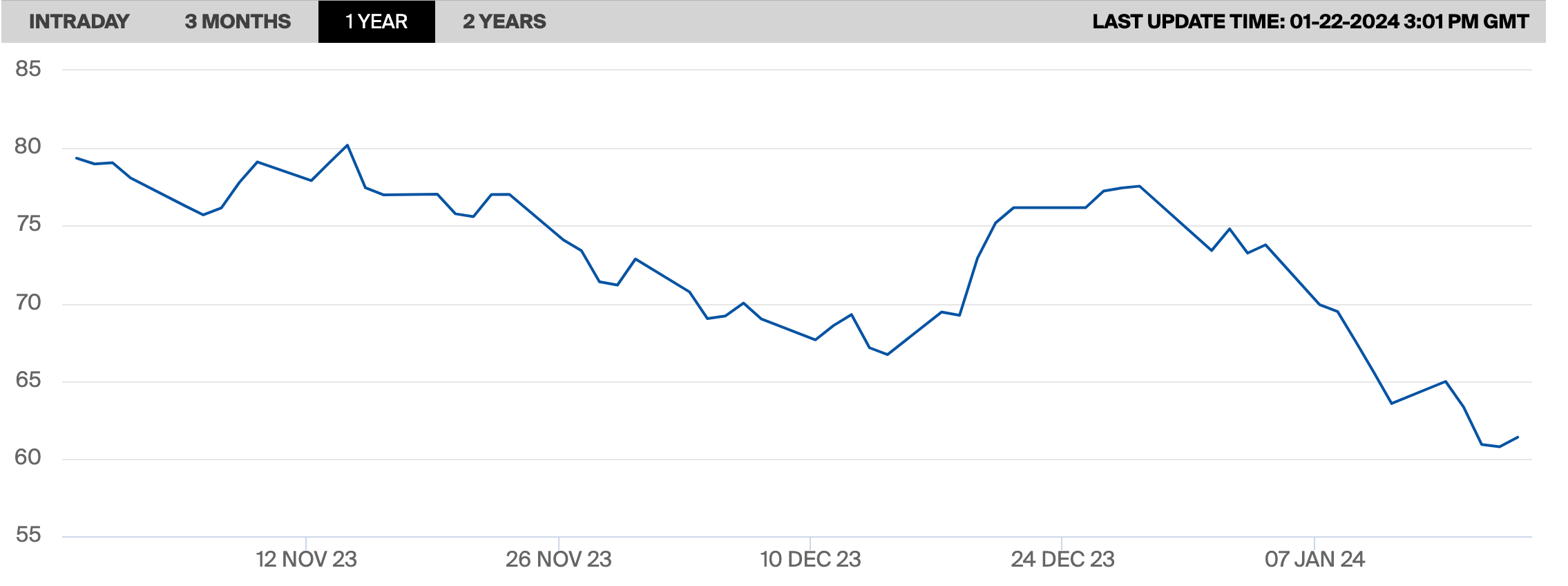

The weekly average EUA prices experienced an 8.26% decrease, falling to €61.52 from €67.06, hitting a two-year low. This trend was mirrored in Monday morning's trading, where EUA prices set a new 17-month low amid minimal buyer presence and almost nonexistent hedging demand. Energy markets also witnessed a decline, contributing to the negative clean spreads.

The EUA weekly short-term price forecast for the coming four weeks is expected to hover between €56.58 and €58.48. This forecast suggests a continued bearish sentiment in the market, possibly influenced by broader economic factors and energy market trends.

The European Securities and Markets Authority (ESMA) reported a mixed picture regarding EUA futures. Open interest in EUA futures at ICE Endex increased by 3.17% between January 5th and 12th, while EEX futures remained steady, decreasing slightly by 0.03%.

UK Allowances: Navigating a Downward Slope

The UK carbon market also faced a downturn. The weekly average UKA benchmark decreased by 9.52%, falling from £38.46 to £34.80. This decline is a significant market correction and may reflect concerns about the UK's future carbon pricing mechanisms post-Brexit.

At ICE Futures Europe, UKA open interest saw an increase of 8.47%, rising from 25.05 million to 27.15 million in the same period. This rise in open interest might indicate growing investor interest or speculative activities in the UK carbon market despite the price decline.

California Carbon Allowances: Gaining Ground Amid Review Updates

In contrast to the EU and UK markets, California Carbon Allowances (CCAs) traded at an all-time high, with the front trades at $41.55. This spike is as the market anticipates updates from the program review. The Intercontinental Exchange (ICE) CCA V24 Front closed at $41.55 on Friday, marking a 1.99% increase over the week.

The weekly trading volume for CCAs was reported at 13.32 million tons, a 24.62% decrease from the previous week. However, the 4-week moving average stood at 17.70 million tons. The Commodity Futures Trading Commission (CFTC) noted an increase in open interest by 4.85 million tons, with compliance entities and managed money increasing their long positions.

Regional Greenhouse Gas Initiative: Above the Cost Containment Reserve

In another significant development, the Regional Greenhouse Gas Initiative (RGGI) allowances traded above the Cost Containment Reserve (CCR) trigger of $15.92. This increase is likely due to expectations of market tightening from the ongoing Third Program Review by RGGI Inc. ICE RGGI V24 Front closed at $16.05 on Friday, up 1.65% week-over-week.

Washington Carbon Allowances: Legislative Changes and Market Response

Washington's carbon market saw a sharp decline in carbon allowance trading, with WCA prices dropping to $45.75. This downturn is attributed to multiple legislative shifts and regulatory uncertainty. House Bill 2376 aims to modify the Climate Commitment Act, impacting carbon allowance allocations for municipal gas utilities. Senate Bill 6058 proposes technical changes in linkage efforts, and a ballot initiative in November threatens to end the cap-and-trade program.

This legislative focus has led to a decrease in trading volumes, with a 936 contracts drop. The week's analysis points to a $1.63 drop in WCA prices, driven by political and regulatory uncertainties.